Jeanne has been building language models since before it was cool.

With nearly ten years of experience in AI, multilingual NLP, and data science, spanning both industry and research, her focus has always been on multilingual and low-resource settings, where data is scarce, noisy, and rarely benchmark-ready. Her work has spanned misinformation detection on social media and real-world language understanding in underrepresented languages, with privacy and data protection as a consistent consideration throughout. More recently, her interests have extended into finance, specifically how language models can be used to extract signal from social media and news to model and anticipate market behaviour.

Her research has been published at ACL, including work on automating multilingual healthcare question answering in low-resource African languages. She approaches problems at the intersection of language, people, and systems, with a particular interest in making AI work in contexts it was never designed for.

Outside of work, she reads widely across behavioural economics, climate change, and misinformation and writes occasionally when something is worth saying.

Originally from Cape Town, Jeanne now lives in England with her husband and two Bengal cats, Eira and Kinzy.

Blog

A Pre-mortem on the Meme Stock Bubble

Fee-free trading platforms, like Robinhood, made it very easy for novice investors to get started with their trader journey. Investors started to coordinate their efforts on Wall Street Bets, implemented short squeezes on dead-beat stocks like GameStop and the rest is history. This article explores the Meme Stock Bubble and the factors that influenced it.

March 9, 2021

Disclaimer: this article does not constitute financial advice.

A speculative bubble is a spike in asset values within a particular industry, commodity, or asset class to unsubstantiated levels, fuelled by irrational speculative activity that is not supported by the fundamentals.

With Fundamental Analysis, we try to determine a stock’s real or “fair market” value using various macroeconomic factors, the company’s revenue streams, balance sheets, and debt obligations, and industry position. The goal is to reach a point where an (intelligent) investor can determine if a company is overvalued or undervalued given its current market price. The belief of fundamental analysis is that eventually the market will correct itself, or return to the “fair market” value, because eventually all investors will realise that a particular stock is either overvalued or undervalued and behave accordingly.

Things you don’t see during a bear market

With speculative bubbles, investors buy stocks because they see the price going up, and not because they necessarily believe it is fundamentally sound. The euphoria of speculative bubbles tend to make investors more irrational and less risk-averse. A belief that an asset class will always defy gravity drives investors to buy more of already-overvalued stocks, thinking there will always be someone willing to buy the asset at a higher price.

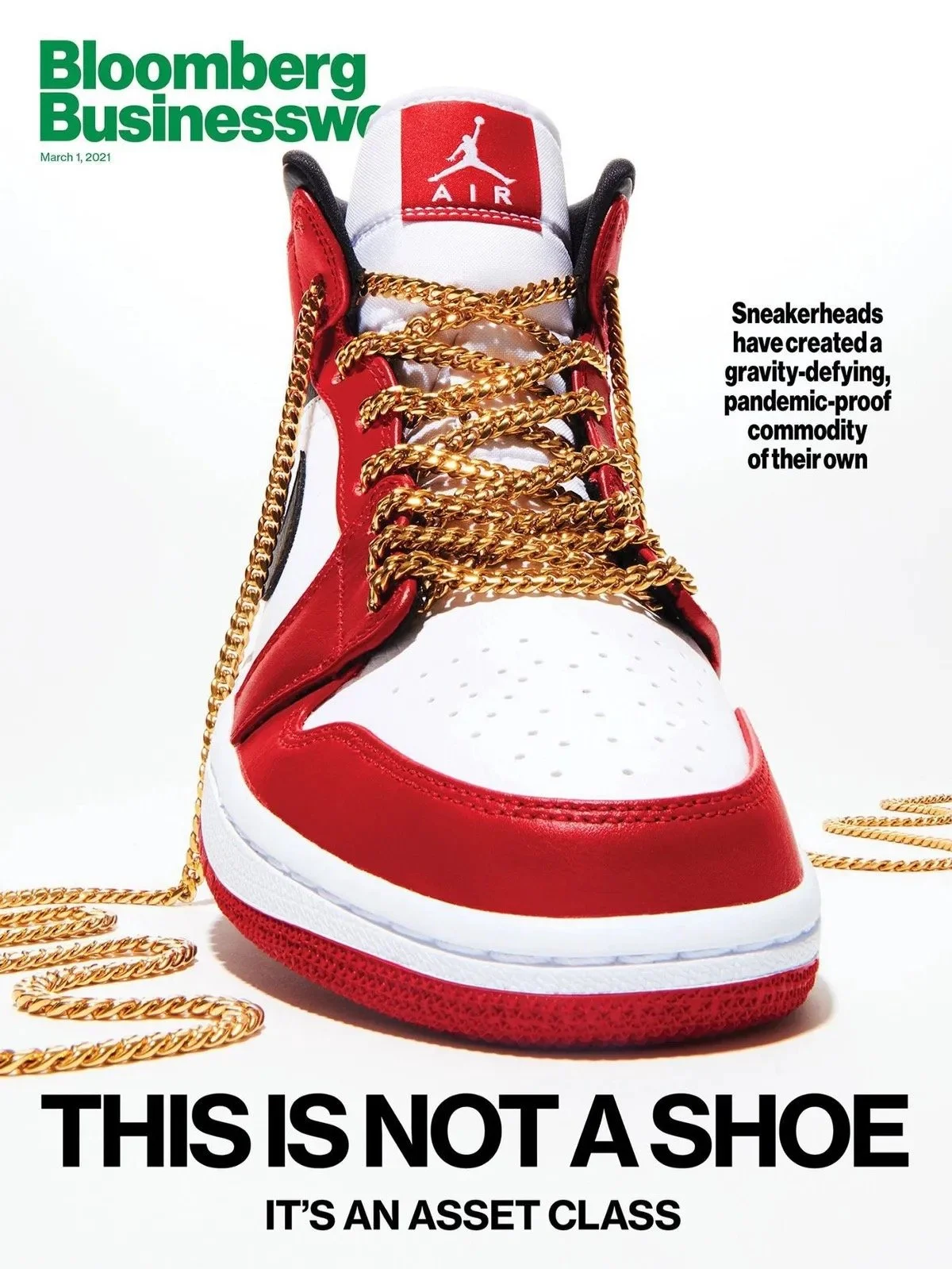

Even the media, the gatekeepers of truth, fall for the euphoria. A sign of the times is this graphic depicting “Sneakers as an asset class”, which I discovered while scouring Twitter. The Tweet simply said, “headlines you don’t see at bottoms”. Here, the “bottoms” refer to periods of negative sentiment in the stock market, where growth is flat or even heading downwards. No one spoke about “gravity-defying asset classes” post DotCom Bubble, that’s for certain.

Meme Stock Mania

Normally, speculative bubbles are notoriously hard to recognize while happening, but seem obvious after they burst. But this one has been glaringly obvious. Its been meme-worthy, to say the least. An early warning sign was the rapid rise of Tesla’s share price, and the cult following that its CEO, Elon Musk started to amass. Between January 2020 and January 2021, Tesla’s share price rose 750%. At some point, its market cap exceeded the combined market cap of the top 9 car manufacturers in the world.

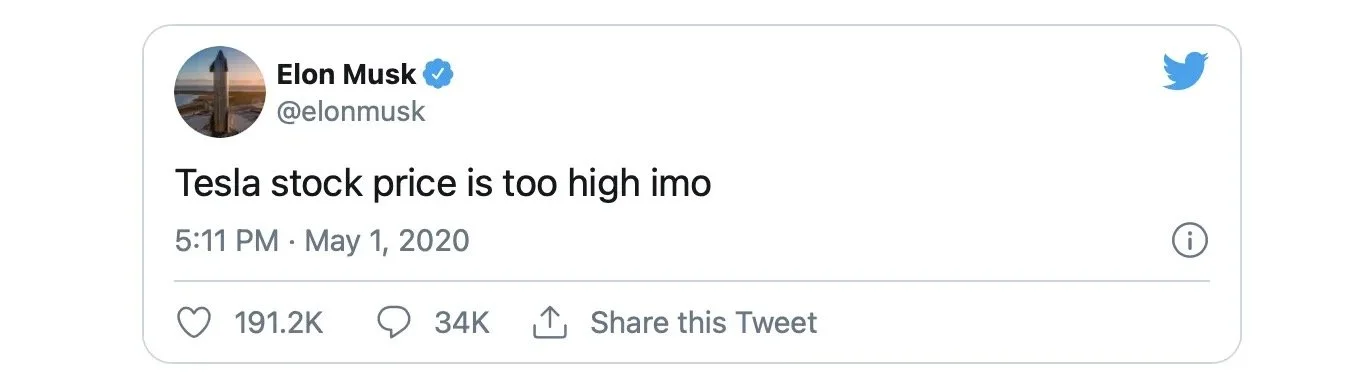

The impact of Musk’s tweets on the stock market revealed how truly bizarre the current investor landscape had become. On May 1, 2020, Elon Musk tweeted the following:

This resulted in Tesla’s share price closing down by 10.3%, on the day. He pulled a similar in June 2020, with similar effect. In August 2018, Musk posted about Tesla “going private, funding secured” at $420 a share. This was just a joke (apparently) but it cost him his role as chairperson. In meme culture, “420” is used to refer to cannabis or to the act of smoking cannabis.

I highlight Tesla because it seems, to me at least, to be the spark of this meme stock bubble. Or at least smoke telling you there’s a fire somewhere. Meme stocks are called as such because its basically for the LOLs. It’s a meme that has gone viral.

How did we get here?

Low yields in money markets have forced investors to look for alternative, more risky instruments to protect their moneys from inflation. That, combined with the additional disposable income that people have because they were sitting at home for the better part of the past year, plus the growing frustrations due to wide-spread job losses, growing debt and grim economic outlooks saw more and more individuals becoming “retail investors”. Fee-free trading platforms, like Robinhood, made it very easy for novice investors to get started with their trader journey. Suddenly, the stock market was being pumped full of money from investors who lived for the most basic form of technical analysis:

Buy cause it’s going up, sell cause it’s going down.

Retail investors piled onto growth stocks like Apple and Amazon, each of which has grown approximately 1200% over the past ten years. Valid thinking — given that these two highly innovative companies have healthy revenue streams and considerable market share— although the sheer force of their collective efforts pushed these stocks into the overvalued region. Apple’s share price more than doubled in less than a year, from a low of $56.87 on March 21, 2020 to a peak of $145.09 on January 15, 2020. Which is fine. It’s a free market, right?

Emboldened by zero-commission trading, less rigorous margin requirements and an app that gamifies trading, meme stock investors evolved their strategy:

Buy because we want to make it go up.

Now, usually small time investors don’t have big influence on market movements, because their small, individual trades are uncoordinated and largely cancel each other out. But what if millions of traders around the world starting sharing notes and coordinating attacks? This is exactly what happened with meme stocks. Retail investors started buying up shares of not-so-fundamentally sound investments, like AMC Entertainment Holdings, BlackBerry, GameStop, and Nokia. What many of these companies have in common is anaemic financials, declining market share, and lacking innovation in the new economy. Wall Street knows this and had rightly shorted many of these meme stocks. r/WallStreetBets knows that Wall Street has shorted many of these stocks, and decided, for no particular reason, that they will be taking on Wall Street.

Take GameStop. GameStop is an American retailer that specializes in video games, consumer electronics, and gaming merchandise. At one point, it was the most heavily shorted stock in the S&P 500. r/WallStreetBets, with literally millions of subscribers, took notice of this stock, with a little help of Michael Burry (the guy from The Big Short movie).

On the 1st of December, Game Stop opened at $19.96. By 28 January, it had peaked at a high of $483.00, a more than 23,000% increase. This Godzilla-sized rally caused a short-squeeze for those who were bullish (Big Money hedge funds and investment firms) on GameStop’s future. From Investopedia, cause I can’t explain it better myself:

A short squeeze occurs when a stock or other asset jumps sharply higher, forcing traders who had bet that its price would fall, to buy it in order to forestall even greater losses. Their scramble to buy only adds to the upward pressure on the stock’s price.

Even Elon Musk got in on the fun, a link to the WallStreetBets thread on GameStop. This brought the GameStop saga to peak exposure, and resulted in a 100% increase in the share price during after-hours trading.

The tweet that made r/wallstreetbets go mainstream

The story does not end there. The stock might have peaked even higher, had Robinhood and other easy-trading platforms not restricted trade on several meme stocks, including GameStop, AMC Entertainment ,and Nokia. A congressional hearing on the events started on 18 February.

No one really understands why WallStreetBets decided to take on some of the most powerful financial institutions in the world. Was it a sophisticated market manipulation strategy, a class war on institutional investors, a long term troll, or just a joy-ride to the moon for the LOLs? “It certainly started as a meme. That’s how WallStreetBets operates,” Jaime Rogozinski, who created the subreddit, told Wired.

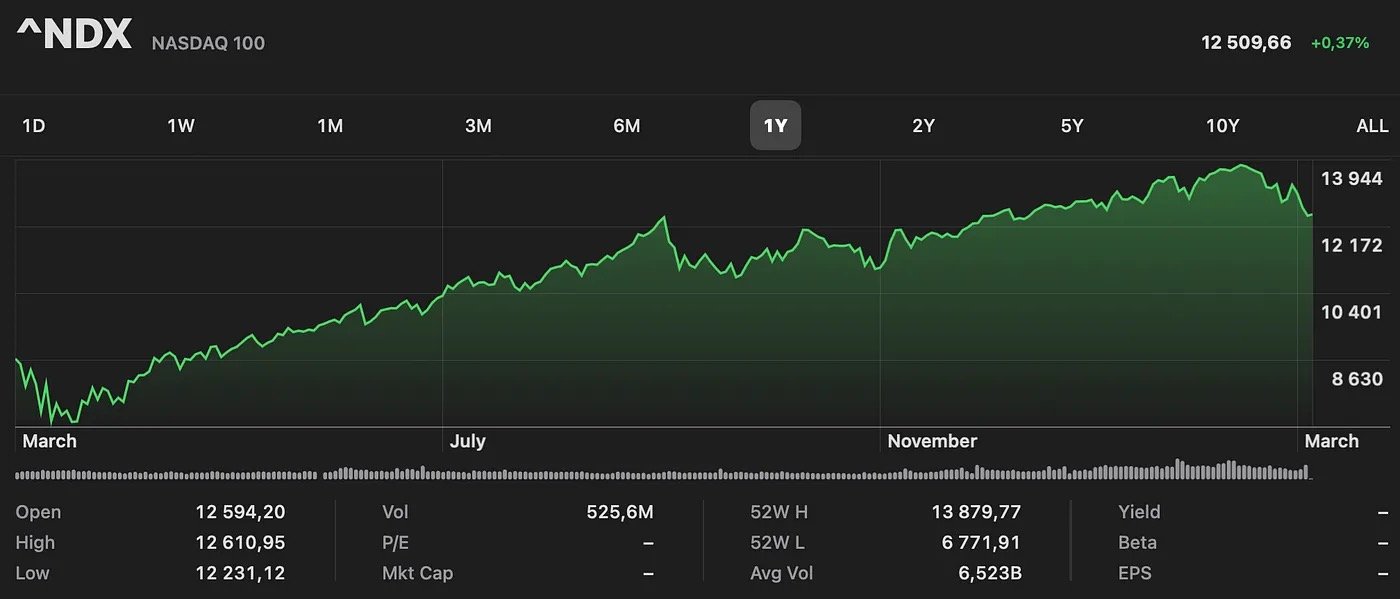

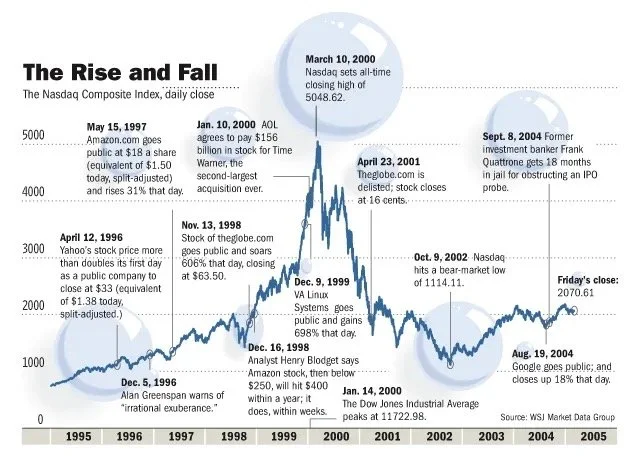

Nevertheless, this reckless behaviour is indicative of a much larger problem. The stock market has, indeed, become violently dislocated from reality. We are certainly in the end game now. One need only look at the charts to understand how nostalgically bizarre things have become. From its lowest point of $6771 to its highest point of $13879 this past year, the Nasdaq 100 essentially doubled in value. The last time the Nasdaq did this was in during the DotCom Bubble.

The Waiting Game

For the past year, believers in fundamental analysis kept looking at the price charts, saying, “It’s gonna come down any day now…”

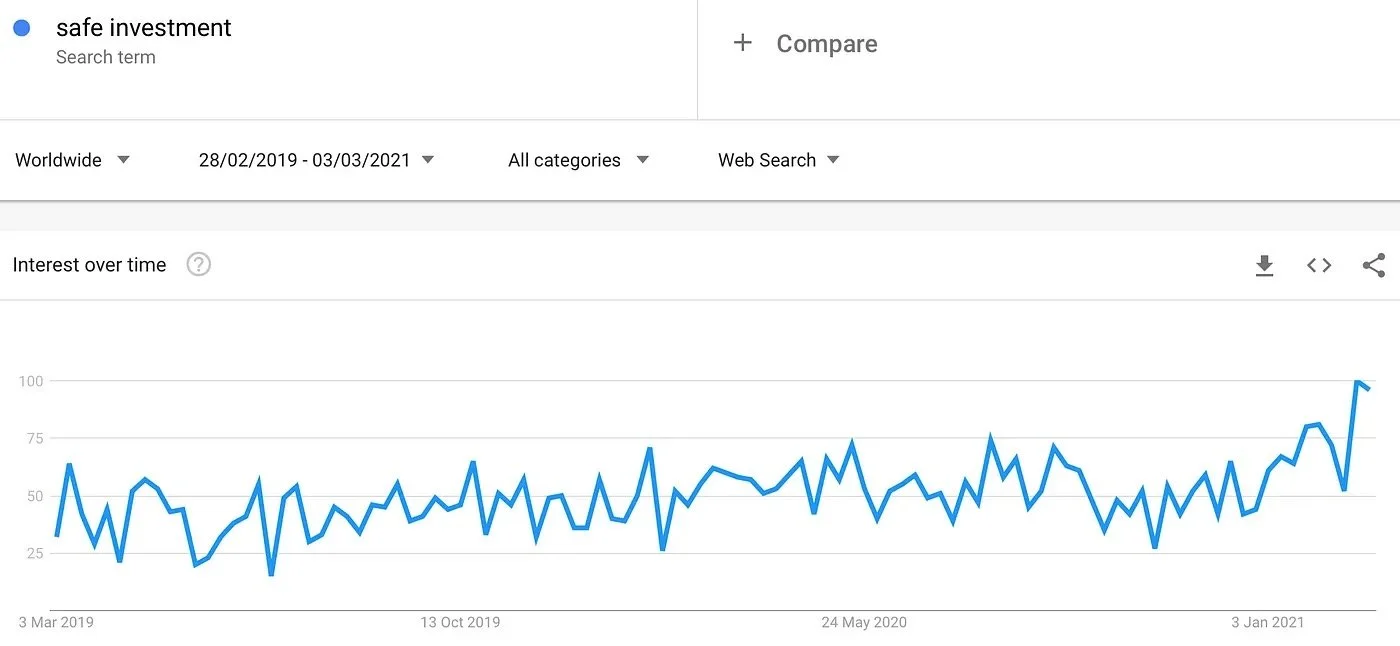

Google Trends serves as a good proxy for what the general population is thinking. It has been used to successfully track outbreaks of viruses in different countries (because people search for symptoms, etc). It can also be used to gauge market sentiment. Right now, the world seems to be desperately concerned with finding “safe” investments to put their money in, should a crash be coming. Search volumes for the term “safe investment” is at its highest in 2 years.

Google search volumes over time for “safe investment”. Created on 03/03/2021 by Author.

Dala what you must, but this graph tells me that investor fear is at an all-time high. And with good reason. All major stocks, including Apple and Amazon have seen massive declines over the last month. Tesla’s epic bull run has seen a decline of 25% over the past month. Even Michael Burry is short on Tesla. Coincidently, he was long on GameStop before the whole short-squeeze saga.

Every bubble in history has popped spectacularly and, more importantly, eventually. We haven’t seen the crazy single-day double-digit declines that ended many of the previous speculative bubbles. But after much a hoo-ha, people seemed to have quietly accepted that the stock market won’t be going up like it used to. Perhaps the madness has finally come to an end.

Closing remarks

For a long time, I have been monitoring the stock market and wondering whether or not we are in a bubble. Bitcoin rising and then the GameStop mania was the final piece of the puzzle. I was in quite a rush to finish this article because I was terrified there would be a massive crash, and then I would have had to think of a new title! For those interested, a pre-mortem is quite literally the opposite of a postmortem/autopsy.

The DotCom Bubble

Following the burst of the DotCom bubble, the surviving companies like Apple, Google, and Microsoft became apex predators in their respective fields. This article explores the factors leading up to and during the DotCom bubble, as well as examine the long-term impact on the tech ecosystem.

June 21, 2020

The iconic San Francisco motel-themed billboards of Yahoo. Sourced from VentureBeat.

I was only about 5 years old when the DotCom Bubble took effect, and while the DotCom Bubble was recent enough to live in most people’s memories and not in the dusty history books, in the technology age 20 years is a millennium. Just look at that billboard, it is practically archaic!

The DotCom Bubble highlighted the pitfalls of greed, over-promising, and ignorance. It also proves an interesting case study for the intricate relationship between innovation, and economic growth.

A DotCom company was called as such because many of them simply consisted of a website. They were online platforms that would facilitate everything from banking to streaming content to buying pet supplies. This was the dawn of the Information Age — an economy built on information technology. The Internet would become as revolutionary as railroads and electricity, bringing people closer together and providing the means of powering new services and markets.

So what preceded the DotCom Bubble?

A number of factors:

The World Wide Web was created in 1989 by Sir Tim Berners-Lee, who wanted to create a globally-connected platform where information can be shared with anyone, anywhere. This sparked the era of globalisation.

Home computers became mainstream — between 1984 and 2000, the percentage of households in the United States with a PC went from 8.2% to 51%.

In 1995, Microsoft Windows 95, which included the first version of the Internet Explorer (another living fossil), went on sale.

A picture begins to form of something that does not grow at a linear pace. Today the Internet is ubiquitous, and we cannot imagine our lives without it.

Jack F. Welch, chairman of General Electric, was quoted in 1999 as saying that the Internet “was the single most important event in the U.S. economy since the Industrial Revolution.”

Back then, the Internet was a very new thing, and people were struggling to grasp its potential. There was anxiety around the commoditization and regulation of the Internet, and there was the fear of the Y2K bug — that computers would misread 2000 as 1900, and that this would cause critical computer systems to collapse. But the Internet was about to revolutionalize we shop, socialize, learn, travel, and more.

Party like its 1999

Although very real and opening up a plethora of new business opportunities, the Internet — combined with free-market economics, low interest rates, and heavy speculation — resulted in a Wild Wild West era for DotComs. It created an over-enthusiastic investor pool that seemingly overnight stopped caring about things like business plans and debt piles. It was also the Internet that enabled buying stocks directly online, which added plenty of less experienced, less sophisticated investors (willing to buy stocks that were overvalued) to the investor pool.

The number of venture capitalist firms also grew by 90% between 1995 and 2000. More money than ever before was made available for startup capital investments. During the same period, 439 DotCom companies went public, raising $34 billion in capital.

Rob Glaser, who founded Progressive Networks in 1994, said, “In 1995 and 1996, if you said you were doing an Internet toaster, I’m sure you could find a venture capitalist to fund it.”

Every tech startup (affectionately identifiable with the .com at the end of their name) was seemingly a unicorn — the next big thing — and everyone had FOMO on the IPO of said unicorn. Many DotCom companies were bandwagon jumpers, with few original ideas, thin business plans, and plenty of big talk. Some spent up to 90% of their budget on advertising to get their brand “out there”.

To add to their net operating losses, they were overpaying average talent and hosting exuberant parties. They also offered their products/services for free or at a discount with the hope that they will create loyal customers whom they can charge profitable rates in the future. The goal was to “get big fast” — identify a niche market early and gain market share as quickly as possible, to shut out all competitors.

Fall from grace

During the early years of the DotCom bubble, investors were willing to forgive DotCom companies for posting losses while they were busy developing their IP and expanding their market share. But after a few loss-making years, investors started to get nervous. Many had become overnight paper millionaires from the skyrocketing IPOs, but as we all should know — share price does not equal fair value nor company performance. Surely the goose will eventually run out golden eggs to lay?

Stock market bubbles, during their ascension, tend to be very sensitive to market shocks. The DotCom Bubble was no different — on March 13, news that Japan had once again entered a recession triggered a global sell-off that disproportionately affected the overvalued technology stocks. This, combined with aggressively-raised interest rates, the events of 9/11, several accounting scandals including that of Enron and WorldCom, sparked a two-year decline in the Nasdaq Composite — comprised overwhelmingly of technology stocks. Many DotCom companies struggled to secure further venture capital, whilst burning through their cash pile. IPOs and further stock offerings was out of the question. Since they were nowhere near profitability and received no cash influxes, they eventually went into liquidation. An estimated 52% of DotCom companies went bust by 2004.

The DotCom bust was a combination of increased scrutiny of DotCom companies’ financials, investor fatigue, and the belief that the Internet was a fad. Of course, the Internet was not a fad, and would soon bring forth a new Fourth Industrial Revolution.

The aftermath

If bubbles popping were extinction-level events, then companies like Apple, Google, and Amazon were the crocodiles of the tech ecosystem. The Big Pop allowed them to become apex predators in their respective fields, for several reasons. Real estate became much cheaper, hardware became easier to obtain, the market was flushed with recently-unemployed, talented software engineers, and the extinction of their competitors allowed them to rapidly gain market share. Today, they are some of the most valuable, and most recognizable brands in the world. Their respective portfolios overlap somewhat and often they compete for market share, as well as talent. In later years, companies like Facebook and Netflix would join their ranks. Within their respective workplaces, each of these tech giants demands extremely high performance from their employees and have a habit of acquiring any potential competition. Collectively, they are called FAANG, and as of January 2020, they have a combined market capitalization of over $4.1 trillion.

Although nearly untouchable today, back then these companies were not immune to the fallout. In the face of diminishing confidence, Amazon’s share price fell from $107 to just $7. Google waited out the DotCom bubble and only launched its IPO in 2004. At the height of the DotCom Bubble, Apple’s share price reached a height of almost $5, only to fall below $1 in 2003.

For Apple, the decade following the DotCom Bubble was most prosperous as it led the innovation of consumer electronics. Apple launched the iPod in 2001 and introduced the iTunes Store in 2003, where users could purchase individual tracks for just $0.99. The iTunes Store hit five billion downloads by June 19, 2008. Apple also released Mac OS X, the primary operating system of Apple’s Mac computers, in 2001. The first iPhone, the integration of an Internet-enabled smartphone and the iPod, was introduced in 2007. And in 2010, they introduced the iPad.

Steve Jobs introducing the first iPhone in 2007.

The innovation that followed the malaise of the early 2000s were led by these apex companies. They invested heavily in new startups and even built the infrastructure (cloud computing) that allowed smaller companies to iterate much faster for much less upfront infrastructure investment.

The DotCom bubble fostered an era of entrepreneurship that has not been seen in the US since before the Great Depression. It provided a petri dish to test out the validity and marketability of a wide range of Internet services. Many of the services were way ahead of their time — like online food delivery and online clothing stores. Unfortunately for these services, the consumer base, technology, and infrastructure simply were not ready.

Today, investors look at tech IPOs with increased scrutiny — the consensus is that one simply does not take a tech company public before it reaches profitability. WeWork, Uber, Lyft — all these companies went public before having showing profitability. They were whipped in the public square — figuratively, of course — with their share prices falling on the day of their respective IPOs.

Closing remarks

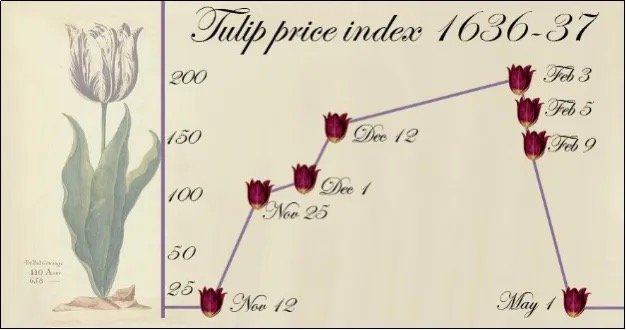

In hindsight, everyone has 20–20 vision. But during a bubble, everyone seems to have these unrealistic, almost fanatical views of what the future would look like. The first recorded speculative bubble dates back to 1636–1637, named the Tulip Mania. At the height of the mania, the bulbs sold for approximately 10,000 guilders — equal to the value of a mansion on the Amsterdam Grand Canal. Investors believed that there would always be a buyer willing to purchase the bulb at a higher price than their entry point. The perceived value of the tulip bulbs became disjointed from their intrinsic value, which was destined for a correction.

Tulip Mania of 1637

While researching the DotCom Bubble, I noted many similarities with today’s manner of market speculation and that of the DotCom Bubble. Trading apps that allow investors to buy fractional shares with zero commission has introduced plenty of young, inexperienced investors to the market, and this has coincided with some of the strangest events in stock market memory. Is history repeating itself? Perhaps the frequency of bubbles coincides with the memory span of investors.