Jeanne has been building language models since before it was cool.

With nearly ten years of experience in AI, multilingual NLP, and data science, spanning both industry and research, her focus has always been on multilingual and low-resource settings, where data is scarce, noisy, and rarely benchmark-ready. Her work has spanned misinformation detection on social media and real-world language understanding in underrepresented languages, with privacy and data protection as a consistent consideration throughout. More recently, her interests have extended into finance, specifically how language models can be used to extract signal from social media and news to model and anticipate market behaviour.

Her research has been published at ACL, including work on automating multilingual healthcare question answering in low-resource African languages. She approaches problems at the intersection of language, people, and systems, with a particular interest in making AI work in contexts it was never designed for.

Outside of work, she reads widely across behavioural economics, climate change, and misinformation and writes occasionally when something is worth saying.

Originally from Cape Town, Jeanne now lives in England with her husband and two Bengal cats, Eira and Kinzy.

Blog

Taking Stock of The AI Landscape - 2 Years since ChatGPT Launched

2 years ago, ChatGPT took the world by storm, being the first true conversational agent. This blog post explores the changes to the AI landscape since, from new competitors to litigation about copyright infringement.

4 November 2024

On November 30, 2022, OpenAI launched GPT-3.5, a Large Language Model (LLM) tuned specifically for instruction-following. It was unlike anything else on the market—a true conversational tool that felt remarkably natural. Within five days, ChatGPT gained one million users, making it one of the fastest-growing consumer apps in history. Three months later, it had surpassed 100 million monthly active users.

In this post, I take stock on how much the world has shifted since ChatGPT’s debut.

A competitive landscape

ChatGPT’s overnight success spawned an entirely new industry of AI model providers and competitors, including Perplexity.ai, Anthropic, Google, Meta, Mistral.ai and more. It’s an arms race of who can produce more tokens for cheaper and at the same time stay at the top of the leaderboard.

Nvidia, the provider of the GPUs necessary to train LLMs, has since the launch of GPT-3.5 in November 2022 seen its share price increase 900%. In contrast to most loss-making AI-first companies, Nvidia has also seen its revenue nearly 5x over the same period of time. As the saying goes, in a gold rush, sell shovels.

Bigger is not necessarily better

In 2022, Forbes predicted that the first 10 trillion parameter model was imminent. However, the opposite trend is happening - companies are refining models to be as small as possible while retaining performance.

Smaller models are crucial for driving adoption amongst consumers and researchers by lowering the barrier to entry in terms of memory and compute requirements. Further, it unlocks the potential to run these models on mobile devices.

Smaller models are also cheaper and faster to run inference on. Take GPT-4o-mini, which OpenAI has said is roughly in the same tier as other small AI models, such as Llama 3 8b, Claude Haiku and Gemini 1.5 Flash. GPT-4o mini achieves an impressive 82% on the MMLU benchmark and currently ranks 3rd on the ChatBot Arena leaderboard. At 15 cents per million input tokens and 60 cents per million output tokens, it is more than 60% cheaper than GPT-3.5 Turbo.

Running out of training data

As the models have gotten bigger and bigger over the years, AI researchers have been looking for new and unexplored piles of data to continue feeding the beast. When we want to quantify the amount of training data, we talk about tokens. According to OpenAI, one token generally corresponds to around 4 characters of text or on average 3/4 of a word for common English text. Different models use different tokenisers so the numbers vary, but you can expect a novel with roughly 75,000 words to consist of 100,000 tokens.

The sheer size of data required to train models like ChatGPT is staggering. For reference, GPT-3 (3.5’s predecessor) was trained on approximately 300 billion tokens. The majority of the internet has already been “mined” and new content is increasingly being placed behind paywalls. According to Anthropic’s CEO, Dario Amodei, there’s a 10% chance that we could run out of enough data to continue scaling models.

Consequently, researchers are now focused on optimizing existing data and exploring synthetic data. This might explain the shift toward smaller, more efficient models. Resources are the death of creativity, and the opposite holds true.

Lawsuits and Concerns

Not everyone is thrilled about AI companies using the internet for training Large Language Models. There has been a number of lawsuits where major companies are suing AI companies for copyright infringement and unlawful use of their data.

News Corp, who owns publications like The Wall Street Journal and the New York Post, is suing Perplexity.ai for reproducing their news content without authorisation and also falsely attributing content to News Corp’s publications that they never actually wrote. They are seeking penalties of $150k per violation.

The New York Times filed a lawsuit against OpenAI and Microsoft in December 2023, accusing them of infringing on its copywriter works in training their LLMs. The lawsuit remains unresolved at time of writing. In October 2024, the New York Times also sent a cease-and-desist to Perplexity.ai, demanding that they stop using their content without authorisation. Perplexity.ai hit back, saying they do not scrape with the intent of building Large Language Models, rather that they are “indexing web pages and surfacing factual content” and furthermore, that “no one organization owns the copyright over facts.”

In January 2023, Getty Images initiated legal proceedings against Stability AI in the English High Court. The lawsuit alleges that Stability AI scraped millions of images from Getty’s websites without consent to train its AI model, Stable Diffusion. The trial is expected to take place in summer 2025.

These lawsuits underscore the mounting tensions over how content is used for training and the industry’s “ask for forgiveness, not permission” approach. In response, more content providers, especially news outlets, are placing material behind paywalls to protect it.

Our expectations as users

Users took to using ChatGPT like ducks to water. Finally we had the virtual assistant that Sci-Fi has been touting for decades. One who could answer all our menial questions without growing bored or annoyed. One who could structure our essays and emails, give us feedback on our writing, and coach us on our interactions with our people. One who can help us plan our next trip, and suggest recipes for the few ingredients in our fridge…

However, as we become accustomed to this ease, our expectations grow. We expect an immediate response and we get frustrated when ChatGPT misinterprets our request. We don’t want to have to go and verify its claims - we’d like a list of sources please. No hallucinations. Don’t sound so preppy. Also, we’d like it to NOT train further models on our conversations. Oh, and please be free, thanks.

We don’t have AGI yet

And probably won’t, for a long time. Let’s just leave it at that.

Conclusions

Now, you might be wondering, was this blog post written by an LLM? I can confirm it was not. I don’t like using it for writing, as I, personally, find its writing rather bland and uninspiring. I do occasionally use it to plan an outline or get feedback on my writing. I see it as a productivity multiplier and a phenomenal research tool, especially since ChatGPT integrated search results and citations.

I am a huge fan of ChatGPT and pay for the subscription. I highly recommend everyone try it out. But keep in mind its limitations: it can be inaccurate, outdated, and prone to hallucinations, and it’s wise not to share confidential data. (Also, disclaimer: I own shares in Nvidia.)

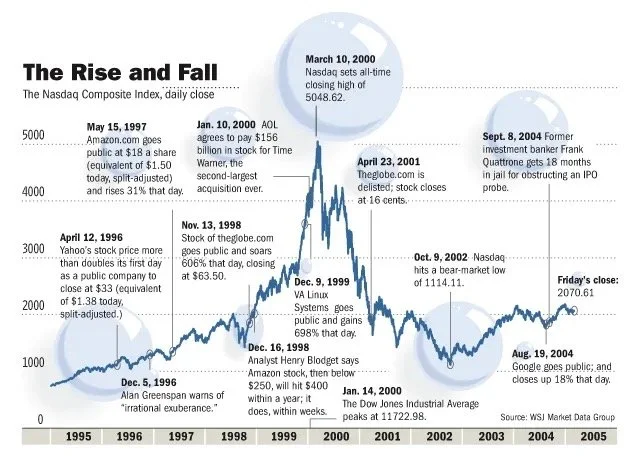

The DotCom Bubble

Following the burst of the DotCom bubble, the surviving companies like Apple, Google, and Microsoft became apex predators in their respective fields. This article explores the factors leading up to and during the DotCom bubble, as well as examine the long-term impact on the tech ecosystem.

June 21, 2020

The iconic San Francisco motel-themed billboards of Yahoo. Sourced from VentureBeat.

I was only about 5 years old when the DotCom Bubble took effect, and while the DotCom Bubble was recent enough to live in most people’s memories and not in the dusty history books, in the technology age 20 years is a millennium. Just look at that billboard, it is practically archaic!

The DotCom Bubble highlighted the pitfalls of greed, over-promising, and ignorance. It also proves an interesting case study for the intricate relationship between innovation, and economic growth.

A DotCom company was called as such because many of them simply consisted of a website. They were online platforms that would facilitate everything from banking to streaming content to buying pet supplies. This was the dawn of the Information Age — an economy built on information technology. The Internet would become as revolutionary as railroads and electricity, bringing people closer together and providing the means of powering new services and markets.

So what preceded the DotCom Bubble?

A number of factors:

The World Wide Web was created in 1989 by Sir Tim Berners-Lee, who wanted to create a globally-connected platform where information can be shared with anyone, anywhere. This sparked the era of globalisation.

Home computers became mainstream — between 1984 and 2000, the percentage of households in the United States with a PC went from 8.2% to 51%.

In 1995, Microsoft Windows 95, which included the first version of the Internet Explorer (another living fossil), went on sale.

A picture begins to form of something that does not grow at a linear pace. Today the Internet is ubiquitous, and we cannot imagine our lives without it.

Jack F. Welch, chairman of General Electric, was quoted in 1999 as saying that the Internet “was the single most important event in the U.S. economy since the Industrial Revolution.”

Back then, the Internet was a very new thing, and people were struggling to grasp its potential. There was anxiety around the commoditization and regulation of the Internet, and there was the fear of the Y2K bug — that computers would misread 2000 as 1900, and that this would cause critical computer systems to collapse. But the Internet was about to revolutionalize we shop, socialize, learn, travel, and more.

Party like its 1999

Although very real and opening up a plethora of new business opportunities, the Internet — combined with free-market economics, low interest rates, and heavy speculation — resulted in a Wild Wild West era for DotComs. It created an over-enthusiastic investor pool that seemingly overnight stopped caring about things like business plans and debt piles. It was also the Internet that enabled buying stocks directly online, which added plenty of less experienced, less sophisticated investors (willing to buy stocks that were overvalued) to the investor pool.

The number of venture capitalist firms also grew by 90% between 1995 and 2000. More money than ever before was made available for startup capital investments. During the same period, 439 DotCom companies went public, raising $34 billion in capital.

Rob Glaser, who founded Progressive Networks in 1994, said, “In 1995 and 1996, if you said you were doing an Internet toaster, I’m sure you could find a venture capitalist to fund it.”

Every tech startup (affectionately identifiable with the .com at the end of their name) was seemingly a unicorn — the next big thing — and everyone had FOMO on the IPO of said unicorn. Many DotCom companies were bandwagon jumpers, with few original ideas, thin business plans, and plenty of big talk. Some spent up to 90% of their budget on advertising to get their brand “out there”.

To add to their net operating losses, they were overpaying average talent and hosting exuberant parties. They also offered their products/services for free or at a discount with the hope that they will create loyal customers whom they can charge profitable rates in the future. The goal was to “get big fast” — identify a niche market early and gain market share as quickly as possible, to shut out all competitors.

Fall from grace

During the early years of the DotCom bubble, investors were willing to forgive DotCom companies for posting losses while they were busy developing their IP and expanding their market share. But after a few loss-making years, investors started to get nervous. Many had become overnight paper millionaires from the skyrocketing IPOs, but as we all should know — share price does not equal fair value nor company performance. Surely the goose will eventually run out golden eggs to lay?

Stock market bubbles, during their ascension, tend to be very sensitive to market shocks. The DotCom Bubble was no different — on March 13, news that Japan had once again entered a recession triggered a global sell-off that disproportionately affected the overvalued technology stocks. This, combined with aggressively-raised interest rates, the events of 9/11, several accounting scandals including that of Enron and WorldCom, sparked a two-year decline in the Nasdaq Composite — comprised overwhelmingly of technology stocks. Many DotCom companies struggled to secure further venture capital, whilst burning through their cash pile. IPOs and further stock offerings was out of the question. Since they were nowhere near profitability and received no cash influxes, they eventually went into liquidation. An estimated 52% of DotCom companies went bust by 2004.

The DotCom bust was a combination of increased scrutiny of DotCom companies’ financials, investor fatigue, and the belief that the Internet was a fad. Of course, the Internet was not a fad, and would soon bring forth a new Fourth Industrial Revolution.

The aftermath

If bubbles popping were extinction-level events, then companies like Apple, Google, and Amazon were the crocodiles of the tech ecosystem. The Big Pop allowed them to become apex predators in their respective fields, for several reasons. Real estate became much cheaper, hardware became easier to obtain, the market was flushed with recently-unemployed, talented software engineers, and the extinction of their competitors allowed them to rapidly gain market share. Today, they are some of the most valuable, and most recognizable brands in the world. Their respective portfolios overlap somewhat and often they compete for market share, as well as talent. In later years, companies like Facebook and Netflix would join their ranks. Within their respective workplaces, each of these tech giants demands extremely high performance from their employees and have a habit of acquiring any potential competition. Collectively, they are called FAANG, and as of January 2020, they have a combined market capitalization of over $4.1 trillion.

Although nearly untouchable today, back then these companies were not immune to the fallout. In the face of diminishing confidence, Amazon’s share price fell from $107 to just $7. Google waited out the DotCom bubble and only launched its IPO in 2004. At the height of the DotCom Bubble, Apple’s share price reached a height of almost $5, only to fall below $1 in 2003.

For Apple, the decade following the DotCom Bubble was most prosperous as it led the innovation of consumer electronics. Apple launched the iPod in 2001 and introduced the iTunes Store in 2003, where users could purchase individual tracks for just $0.99. The iTunes Store hit five billion downloads by June 19, 2008. Apple also released Mac OS X, the primary operating system of Apple’s Mac computers, in 2001. The first iPhone, the integration of an Internet-enabled smartphone and the iPod, was introduced in 2007. And in 2010, they introduced the iPad.

Steve Jobs introducing the first iPhone in 2007.

The innovation that followed the malaise of the early 2000s were led by these apex companies. They invested heavily in new startups and even built the infrastructure (cloud computing) that allowed smaller companies to iterate much faster for much less upfront infrastructure investment.

The DotCom bubble fostered an era of entrepreneurship that has not been seen in the US since before the Great Depression. It provided a petri dish to test out the validity and marketability of a wide range of Internet services. Many of the services were way ahead of their time — like online food delivery and online clothing stores. Unfortunately for these services, the consumer base, technology, and infrastructure simply were not ready.

Today, investors look at tech IPOs with increased scrutiny — the consensus is that one simply does not take a tech company public before it reaches profitability. WeWork, Uber, Lyft — all these companies went public before having showing profitability. They were whipped in the public square — figuratively, of course — with their share prices falling on the day of their respective IPOs.

Closing remarks

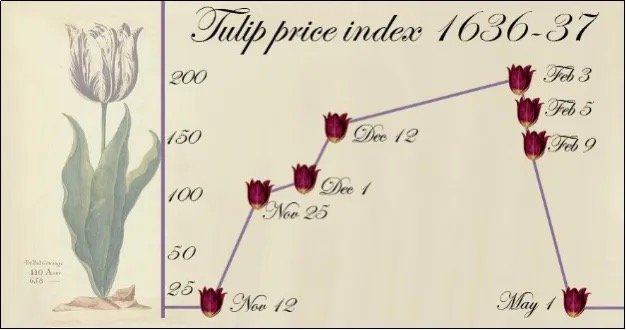

In hindsight, everyone has 20–20 vision. But during a bubble, everyone seems to have these unrealistic, almost fanatical views of what the future would look like. The first recorded speculative bubble dates back to 1636–1637, named the Tulip Mania. At the height of the mania, the bulbs sold for approximately 10,000 guilders — equal to the value of a mansion on the Amsterdam Grand Canal. Investors believed that there would always be a buyer willing to purchase the bulb at a higher price than their entry point. The perceived value of the tulip bulbs became disjointed from their intrinsic value, which was destined for a correction.

Tulip Mania of 1637

While researching the DotCom Bubble, I noted many similarities with today’s manner of market speculation and that of the DotCom Bubble. Trading apps that allow investors to buy fractional shares with zero commission has introduced plenty of young, inexperienced investors to the market, and this has coincided with some of the strangest events in stock market memory. Is history repeating itself? Perhaps the frequency of bubbles coincides with the memory span of investors.